Fitch Ratings has a ‘neutral’ outlook for North American life insurers for 2026 despite a more challenging backdrop, as strong capital, prudent asset/liability management, and liquidity will help issuers to withstand declining policy rates, slowing economic growth, heightened macroeconomic volatility, and geopolitical uncertainty.

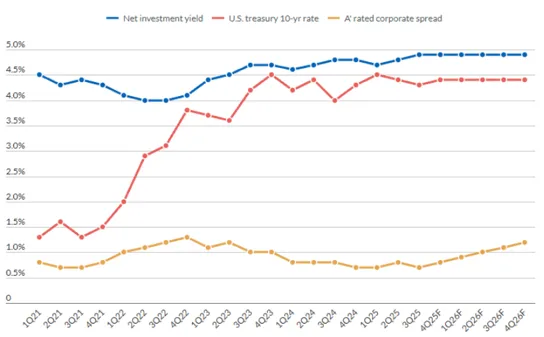

Stability of operating earnings, net investment income and return on equity will be supported by increasing assets under management, improving fixed-income returns, and spread widening that will be partially offset by policy rate declines and equity market volatility. US life insurers are exposed to changes in interest rates, though the sector’s closely matched assets and liabilities partially mitigate impacts.

We expect a modest increase in credit losses YoY and will continue to monitor investment quality and underwriting for signs of late cycle behavior and outsized risk taking. In the event of a more severe market downturn, which is not in our base case, insurers’ strong capitalization will partially insulate balance sheets.

Commercial real estate (CRE) exposure, notably in office properties, will remain under pressure, though it is abating, driven by increased transactions and lower interest rates. Insurers’ credit loss reserves have increased meaningfully, reflecting the challenging dynamics, which should absorb the expected uptick in realized losses.

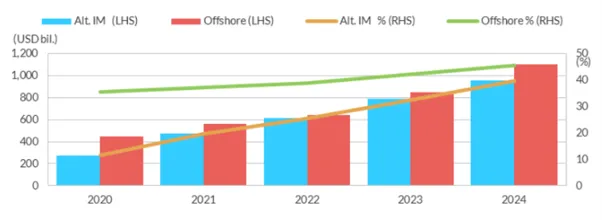

We expect investment risk for the industry to increase modestly in 2026, with growth in offshore reinsurance and partnerships with alternative investment managers (Alt IMs) to persist. US life insurers looking for higher yields and longer-term returns have raised their allocations to private credit and Level III assets but are not expected to face widespread rating pressure if private credit performance weakens over the next 12-24 months. Alt IM partnerships will be tilted towards strategic partnerships, minority stakes, reinsurance platforms and sidecars, with most large Alt IMs having an insurance platform in place.

Figure 1: US Life Insurer Yields and Spreads

Source: Fitch Ratings, company financials, BofA Merrill Lynch, FRB St. Louis.

The continued shift toward less-liquid investments will increase regulatory scrutiny to ensure that the capital held is commensurate with risk. The focus on private credit will increase, particularly among bank and insurance regulators, given the potential spillover risks from the growing interconnectedness among market participants. The National Association of Insurance Commissioners in the United States and the Bermuda Monetary Authority have proposed and adopted initiatives, such as strengthening disclosure granularity and capital requirements, to increase transparency and resilience and protect policyholder obligations.

Figure 2: Offshore and Alt. IM Reinsurance Growth (Reserve Credit and Modified Coinsurance Reserves)

Source: Fitch Ratings, company financials, S&P Capital IQ Pro

The rapid growth of private letter ratings (PLRs) raises risks for US life insurers as the industry increases exposure to more complex, opaque investments untested by a macroeconomic downturn. Key watch items include effectiveness of impending regulation, percentage of capital invested in PLR-rated issuers, illiquidity, and valuation methodologies regarding governance, subjectivity, reliability, and transparency.

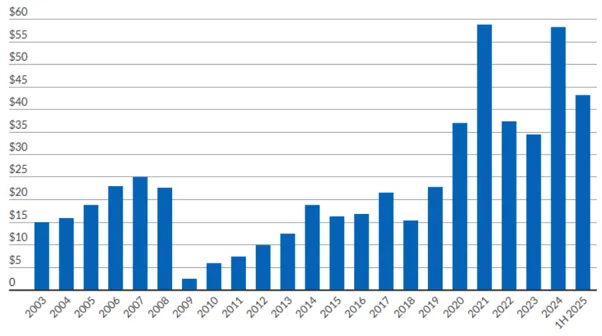

Positive market conditions have supported record issuance of funding asset backed notes (FABNs), with increased issuer participation and investor demand. Robust issuance should continue in 2026, the volume and pace of which will depend on the path of interest rate cuts and credit spreads. Due to their credit sensitivity, rate exposure and commoditized nature, FABNs introduce incremental risk compared to traditional insurance liabilities, with outsized issuance levels marginally increase credit risk in a benign but volatile environment.

Figure 3: US Life Insurer FABN Issuance (USD $bn)

Source: Fitch Ratings, Bloomberg Financial.

We expect offshore (re)insurance activity to continue growing in 2026 as insurers seek to increase reported capital and earnings via spread-based transactions. This can elevate counterparty credit risk. Fitch evaluates reported capital using the Prism capital model on a consolidated basis, which limits the scope for regulatory arbitrage to affect assessed capital strength and credit profiles.

Jamie Tucker, CFA, CPA is a Senior Director in the Insurance Team at Fitch Ratings

Jack Rosen is a Director in the Insurance Team at Fitch Ratings

Any views expressed in this article are those of the author(s) and may not necessarily represent those of Longevity & Mortality Investor or its publisher, the European Life Settlement Association