The 2024 edition of the Life Insurance Fact Book – the American Council of Life Insurers (ACLI) annual review into the inner workings of US-based life insurance company balance sheets – was published in early November. As with last year, I will be highlighting some notable and interesting takeaways from the Fact Book for a series of articles for Life Risk News, starting with this one, a review of key statistics for the life insurance industry in general and some that have relevance for the life settlement industry in particular.

General Industry Performance in 2023

The number of active life insurers in the US continued its decline from 727 in 2022 to 719 in 2023 as further consolidation and, for mutuals, demutualisation, continues to be popular so that they can access additional capital. Total assets of life insurers rose from $8.27trn to $8.74trn (+6.7%) whilst total liabilities rose from $7.79trn to $8.23trn (+5.7%).

This gap in growth between assets and liabilities unsurprisingly led to a rise in Capital Ratios (CR) – those which measure straight surplus. The CR, including the Asset Valuation Reserve (AVR, a reserve to smooth changes in asset prices) changed from 10.5% to 10.7% and, excluding the AVR, from 8.9% to 9.0%.

The AVR, which moves up or down to smooth both variable credit and equity asset price movements, rose 13.1% in 2023 to an aggregate $99bn whilst its sibling, the Interest Maintenance Reserve (IMR), which covers fixed income investments, shrunk 36.3% to $15bn. These movements should not be unexpected in a year when US equity prices rose and bond prices continued to fall further, although the final year-on-year change was not as marked as it would have been if yields remained as high as they were in October 2023.

Life Insurance Products

For life insurance products the picture was one of stasis.

Individual policy in-force face amounts were $13.98trn at the year-end, marginally down from $14.02trn (-0.3%), with aggregate group policy face rising 5.3% from $7.39trn to $8.10trn. In total, all life policy in-force face changed from $21.61trn to $22.15trn (+1.6%).

Despite the fall in individual policy face amount, policy reserves all rose. For individual policies, reserves rose 1.6% from $1.630trn to $1.656trn and group business reserves changed from $0.189trn to $0.194trn.

Premium income on life products was less robust, falling from $170bn to $122bn during the year (-28.2%), which is a notable drop.

Claims paid in individual contracts rose over the year in aggregate. Contractual payments from death claims were slightly down from $67.8bn to $66.3bn (-2.2%) but surrender payments rose from $28.8bn to £35.8bn (+24.1%). Although a much smaller group by value, surrenders on group policies rose from $1.1bn to $5.8bn, a significant rise of 447%.

These surrender statistics are underpinned by the rise in individual policy lapse rates in 2023 to 7.3% from 5.7% whilst those for group contracts dropped slightly from 3.9% to 3.8%.

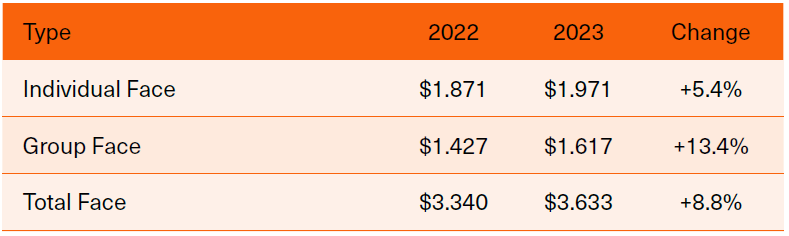

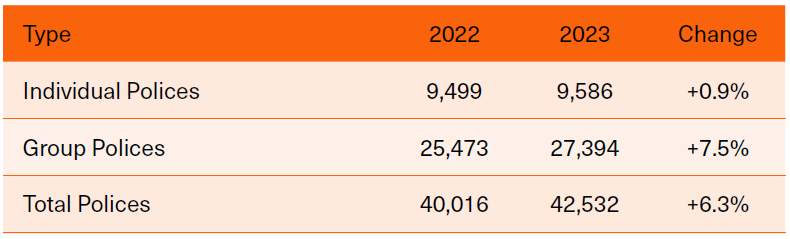

New business, ignoring a tiny amount of credit insurance, on the other hand was surprisingly buoyant. New life products issued by number and face are shown in Figures 1 and 2 below:

Table 1: New US Life Insurance Business by Face Amount, 2023 ($trns)  Source: ACLI Life Insurer’s Fact Book, 2024 Edition

Source: ACLI Life Insurer’s Fact Book, 2024 Edition

Table 2: New US Life Insurance Business by Type, 2023 (000s)  Source: ACLI Life Insurer’s Fact Book, 2024 Edition

Source: ACLI Life Insurer’s Fact Book, 2024 Edition

We will look at these figures in more detail in future issues of Life Risk News. However, the immediate take away from them is that the life insurance industry is experiencing continued growth, with new life products showing growth for both individual and group face amount, and policy numbers. Notably, group policies have seen a significantly larger increase compared to individual policies.

This upward trend in the aggregate face value of policies could be attributed to inflationary pressures during this period, as policy owners adjust coverage amounts to reflect the changing economic landscape. Additionally, the increase in policy count might be partially driven by population growth, as more individuals and employers seek to secure financial protection. .

The drop in death benefits paid out, as shown in Table 3 below, is likely down to the drop off in the Covid-19 effect. The ACLI yearbook includes mortality rates, but a further year in arrears (2021 has only just been added) and these, together with those from 2020, are markedly higher than in 2019.

Table 3: Death Rate per 1,000 Americans

Source: ACLI Life Insurer’s Fact Book, 2024 Edition

Most readers will already be fairly up to date with the rise and fall of Covid-19 deaths, but it is interesting to see that the death rate rose almost 20%, which is around the worldwide estimate of the addition to normal mortality that early Covid-19 added, and as we also know, the effect has dropped off, which helps explain why death claims were lower in 2023 than 2022.

Annuity Business

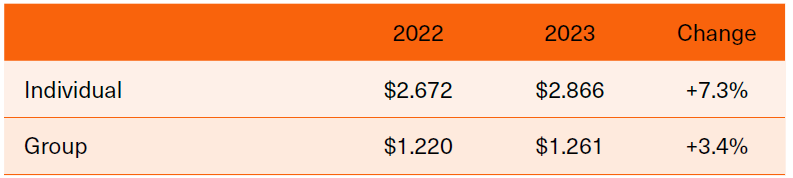

Finally, a shorter summary of the figures for annuities. Annuities represent approximately two-thirds of life insurers’ reserves and so remain important.

Net new contributions (purchase monies and regular contributions) saw a huge change:

Table 4: US Life Insurance Company Net New Contributions, $bns

Source: ACLI Life Insurer’s Fact Book, 2024 Edition

Table 5: US Life Insurance Company Annuity Reserves, $trns

Source: ACLI Life Insurer’s Fact Book, 2024 Edition

The figures for policy reserves merely stand to underline that this is a growing business line as more people join the retired pool. What does stand out is the big revolve for new contributions, with group business shrinking and individual business growing by almost equal and opposite amounts. This year’s effect is not just explained by the runoff of corporate defined benefit (DB) pension schemes to more individually held DC policies like 401(k)s, but something more novel. DB schemes would seem to be securing retirees pensions with annuities in former scheme members own names, as well as possibly topping up early retirement pensions from company funds to facilitate redundancies.

It is therefore better to look at new contributions in aggregate and the picture remains one of steady growth and significance to insurers.

Conclusion

Arguably, the US life insurance industry had a strong 2023 from a balance sheet perspective. Asset growth outpaced liability growth, and policy reserves grew as well and the legacy of the Covid-19 pandemic would appear to be diminishing. After a year in which a significant news item emerged in the life settlement market in particular with the entering of PHL Variable Life Insurance Company into rehabilitation, the overall picture of life insurers as a risk counterparty appears on solid ground.

Roger Lawrence is Managing Director at WL Consulting

Any views expressed in this article are those of the author(s) and may not necessarily represent those of Life Risk News or its publisher, the European Life Settlement Association